Chilean Copper Industry: 3rd Quarter Report

- Punta El Monte

- 6 nov 2023

- 4 Min. de lectura

As Chile continues to play a pivotal role in global mineral production, Punta El Monte offers a complete overview of one of the world's most prominent mining hubs. Providing a deeper understanding of the industry's current landscape and future prospects; exploring key trends, challenges, and opportunities that define this dynamic sector.

GENERAL OVERVIEW - OCTOBER 2023

The political agenda of the past few weeks has centered on the final stages of drafting the new constitutional text, which will face a plebiscite on 17th December. The most contentious rules have been eliminated, and conservative parties are currently most comfortable with the proposal due to its focus on the right to property, the subsidised role of the State, and freedom of choice.

While current polls imply a majority of voters disapprove of the proposal, political analysts anticipate a potential shift in public opinion after the completion of the drafting process and the initiation of campaigning about a month before the plebiscite.

Overall, the gap has been diminishing, with 53% against compared to 28% in favour as of mid-October, versus 59% against compared to 21% in favour in mid-September, as reported by pollster Cadem.

If the approval option prevails, Chile stands to gain an enhanced political system and a bolstered economic organisation. Conversely, the alternative outcome would affirm a constitution that has facilitated Chile's steady progress.

Currently, the Central Bank's Economist Survey projects a 0.4 contraction in the economy in 2023 and a 1.8% expansion in 2024. The Business Confidence has increased in the last three months, currently standing at 43.38 points, its highest level since mid-2022.

ECONOMIC SCENARIO

Economy experienced a 0.5% mom SA contraction in August following two months of expansion. The contraction was influenced by a teachers' strike. Advanced indicators suggest that production would rebound in September, avoiding a technical recession in the third quarter.

Inflation had an annual variation of 5.1% in September, below the 5.3% seen in August. Overall, a sustained disinflation process is observed, anchored in a still-restrictive monetary policy.

It is forecasted that the price variation will be 4.2% by the end of this year -despite the depreciation of the currency in recent months- and is expected to be at 3.0 by the end of next year. This will bring the CPI variation back to the targeted range.

The Central Bank has started to reduce the monetary policy rate recently. There was a first cut of 100 bps in July, another of 75 bps in September and 50 bps at the end of octubre to leave it at 9.00%.

By the end of the year, the market expects it to be 8.00%. However, the final path is subject to a degree of uncertainty because of the exchange rate depreciation.

The current account's consolidation process continues, revealing a 4.5% of GDP deficit at the end of Q2, compared to -6.6% in the previous quarter. Projections suggest a 3.4% of GDP deficit by year-end, though the 17% exchange rate depreciation since June could potentially decrease the deficit even further.

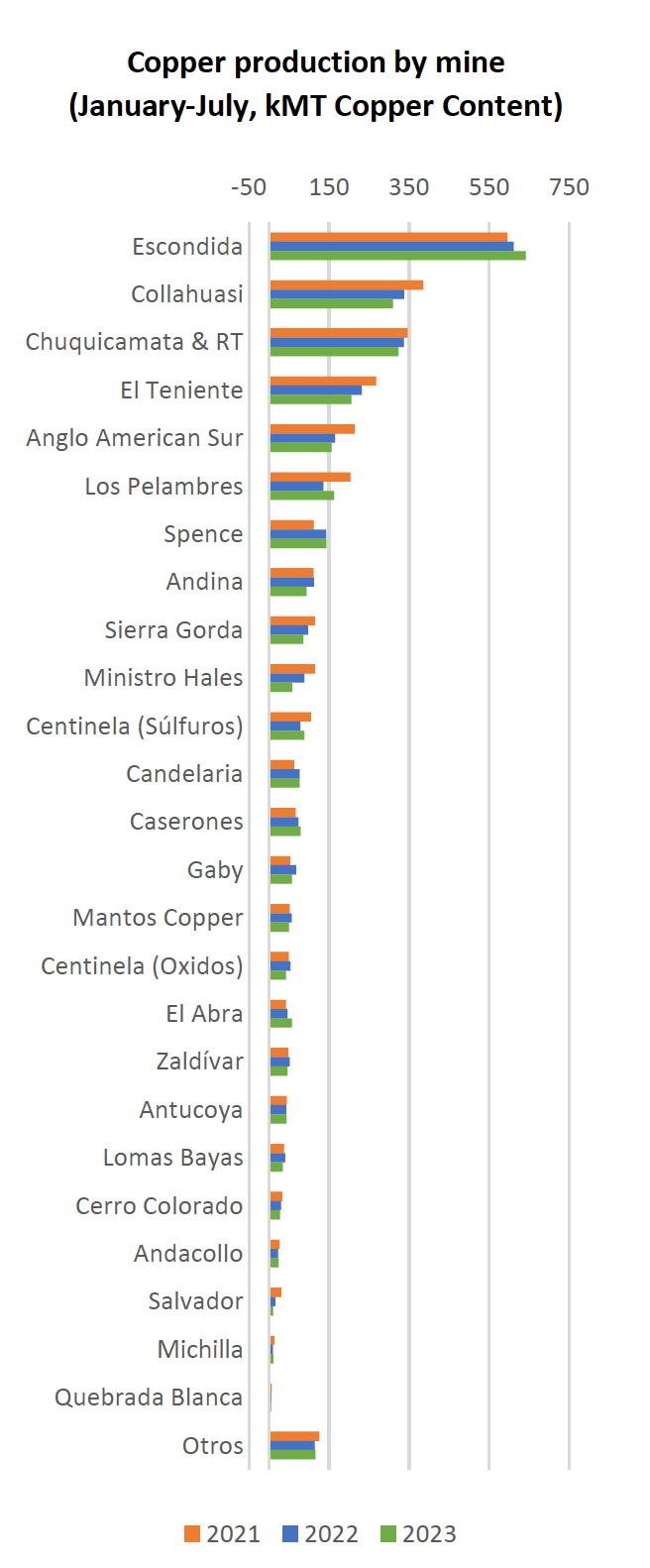

COPPER SECTOR OVERVIEW

Copper production rose by 3.4% YoY in August.Production growth was observed to be at 1.7% YoY in the June-August quarter, as per the latest trends. The sector's performance has seen a revival, which should be bolstered by increased levels of investment, which have been slow thus far.

Investment in mining machinery and equipment has rebounded with an average of USD 144 million in the July-September quarter - a 7% increase compared to the previous quarter. Exports of concentrates averaged of USD 2,091 billion during the same period, rising by 4.9%. In contrast, cathode shipments averaged USD 1,410 million in July-September -a drop of 0.4% from the previous quarter.

During the current economic downturn, there has been a level of stagnation in the job market across the country. Meanwhile, employment in the mining industry has been slightly more volatile.

In the June-August quarter, there was a decline of 5.8 in national salaries and 5.9 in salaries in the mining sector, both measured in USD. This is due to the CLP depreciation being greater than the nominal wage growth.

MINING INVESTMENT IN CHILE

Mining investment in Chile rose to USD 20,038 million for the 2023-2027 period, marking a nearly 30% boost from the previous quarter's figures.

Nonetheless, a part of the adjustment can be attributed to Codelco's project rescheduling.

COPPER MARKET

The monthly average of copper price is currently hovering around cUSD 363 per pound. Market conditions proved to be volatile and a decrease of 4.75% was observed during the period the last three months.

Copper supply and demand growth projections have been revised downwards this quarter. Refined copper supply is now estimated to grow only by 0.9% in 2023 and 4.0% in 2024 (previously 1.5% and 4.7%, respectively). Copper demand is expected to increase by 0.8% this year and 3.1% next year (previously 2.2% and 3.0%, respectively).

Finally, the cash cost of production increased by approximately cUSD 45.5 per pound in 1Q23 compared to 1Q22. The greatest rises were noted in Other Expenses and Services, with around cUSD 41.5, followed by remunerations, with approximately cUSD 8.7, and electricity, with circa cUSD 4.5.

Comments